Takings Clause Victory Would Not Fix Michigan’s Tax Foreclosure System

Cases challenging the constitutionality of government profits from foreclosure sales distort real sources of injustice.

Update: In July 2024, the Michigan Supreme Court held that its holding in Rafaeli v. Oakland County — that a government keeping surplus proceeds from a tax foreclosure auction is an unlawful taking under the state constitution — applies retroactively.

In 2014, Uri Rafaeli underpaid his Southfield, Michigan, property taxes by $8.41. This trivial oversight led the county treasurer to foreclose and auction his home, netting approximately $24,000 in profit — which it kept for the county coffer.

Rafaeli’s story is not an anomaly but a feature of Michigan’s tax foreclosure system since its creation in 1999. The Michigan Supreme Court took on this issue in 2020 in Rafaeli v. Oakland County, determining that government violated the state constitution’s Takings Clause when it kept excess tax sale profits from a foreclosure. In 2023, a similar case out of Minnesota reached the U.S. Supreme Court, where the justices unanimously ruled that local governments cannot profit from property seized to satisfy a public debt.

Now, in Schafer v. Kent County, the Michigan Supreme Court is considering whether its ruling in Rafaeli should apply retroactively, potentially obligating counties to refund hundreds of millions in “windfall profits” from past auctions.

The Pacific Legal Foundation, which represented both Rafaeli and the plaintiff in Schafer, has portrayed these cases as tales of disproportionate government profit from private property, in which victories mean past wrongs have been corrected and justice done. The reality, however, is more complicated — and grimmer. The real engine of profit for counties isn’t the occasional auction windfall but the statutory 18 percent interest (compounded annually), penalties, and fees paid by delinquent taxpayers in the state.

In Rafaeli, the court noted it had consistently upheld “fundamental principles — that the government shall not collect more taxes than are owed, nor shall it take more property than is necessary to serve the public — [to] protect taxpayers and property owners alike from government overreach.” Even the Magna Carta recognized “tax collectors could only seize property to satisfy the value of the debt payable to the Crown, leaving the property owner with the excess,” the court said. Accordingly, property owners had a vested right under the state’s common law to collect surplus proceeds from the tax-foreclosure sale of property.

But nothing in Rafaeli challenged delinquent tax payments made before foreclosure. As Rafaeli’s attorney said during oral arguments before the Michigan Supreme Court, “Rafaeli . . . [is] not challenging the statutory interest or penalties or fees that are tacked onto their property tax debts.”

Discussing the case in 2020, attorneys from the Pacific Legal Foundation argued that finding in favor of Rafaeli would “remove that perverse incentive for government to be foreclosing over an $8 debt.” This ignores the stronger source of perverse incentives: the interest, penalties, and fees that accrue before a foreclosure. After all, the government can choose not to foreclose and sell, instead keeping property owners perpetually indebted and paying.

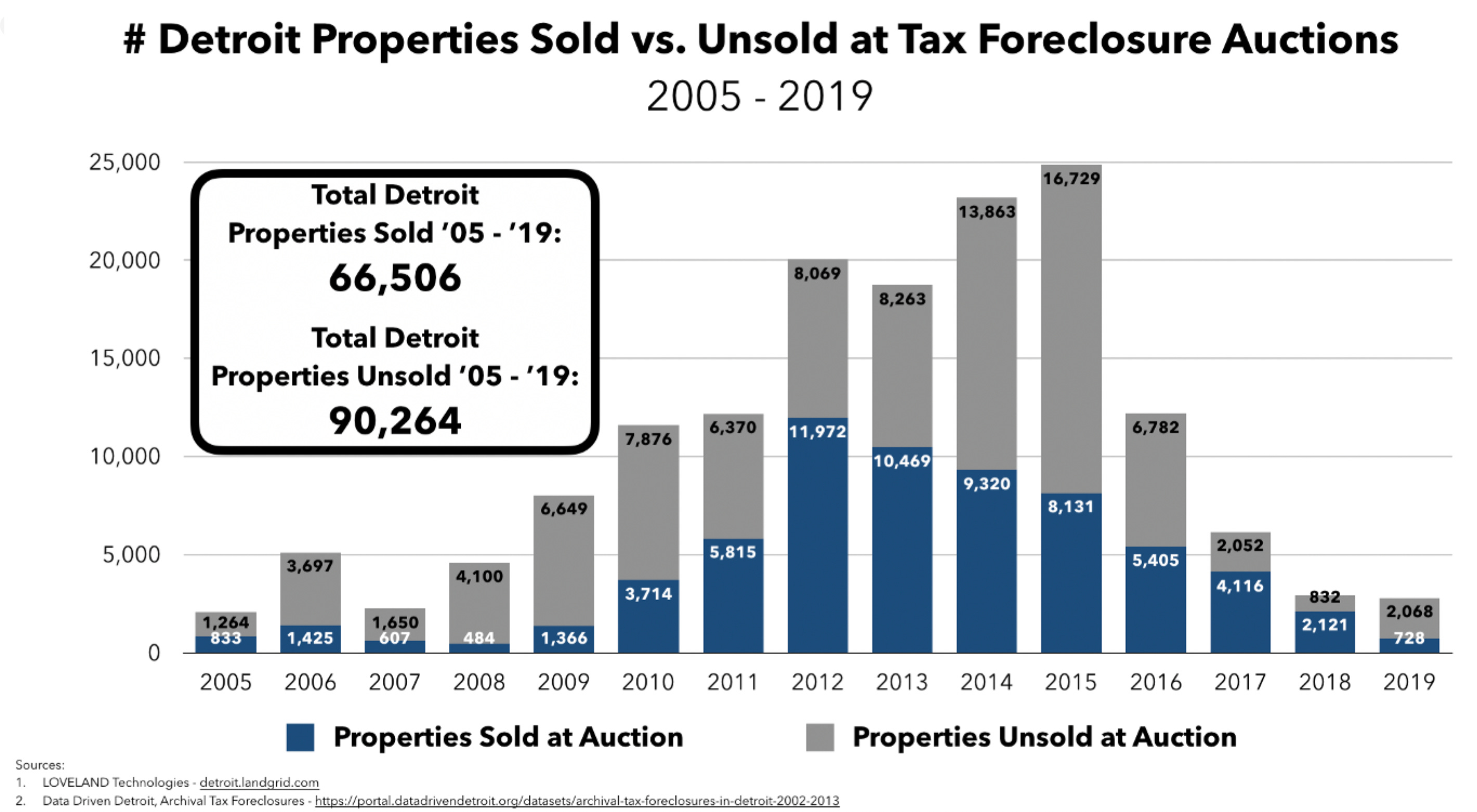

Consider Wayne County, the state’s largest county and home of Detroit. It has been the epicenter of tax foreclosure in Michigan for more than 20 years. One in three Detroit properties have gone through tax foreclosure since 2005, more than 150,000 properties total. Despite having only 7 percent of Michigan’s population, Detroit was home to 60 percent of statewide tax foreclosures in the 2010s. Tens of thousands of the city’s homeowners have lost their homes to tax foreclosure.

As a result, analysis of the Wayne County treasurer’s delinquent tax profits from 2012 to 2016 shows a significant influx of funds from two main sources related to delinquent property taxes. First, the office collected $56 million in windfall profits from properties that were sold at tax foreclosure auctions. Second — and far more substantially — was $159 million in profits from property owners who made payment on their overdue taxes before their properties reached the auction. This larger sum includes not only the back taxes but also additional interest, penalties, and fees mandated by state law.

While this data reflects only one county and a subset of tax foreclosure years it is likely this is a pattern found statewide: There are always going to be far more delinquent taxpayers than there are property owners who actually wind up in tax foreclosure. Statewide, seven times more properties fell into tax forfeiture (a stage reached after 18 months of tax delinquency at which point additional interest on the delinquency is assessed and properties are prepared for eventual tax foreclosure a year later) than went to a foreclosure auction between 2011 and 2018. But the rights of the owners of these properties are not impacted by Michigan’s recent takings litigation.

Further, a ruling that Rafaeli applies retroactively would not make whole most former homeowners whose homes were sold in foreclosure. Instead, the primary beneficiaries are likely to be speculators, landlords, and financial institutions who owned portfolios of tax-foreclosed properties across which multiple instances of windfall profits could be owed.

During oral arguments in Schafer, the plaintiff’s attorney argued “most of these people lost absolutely everything when they lose their homes” and that retroactivity would provide former owners “with what’s constitutionally required.” But, as the attorney herself acknowledged to the court, “these properties are sold at bargain basement prices in the auctions.” Indeed, more than half of the 150,000 Detroit properties tax foreclosed over the last 20 years did not sell at auction even for the minimum bid price of $500. When a property is sold at auction for less than the tax debt owed, or does not sell at all, there are no profits generated and nothing to return to a former owner.

{kind=link}

Speculators and landlords, on the other hand, often saw entire portfolios of properties tax foreclosed. Why? It was part of their business model.

Rather than viewing rental properties as assets in and of themselves, landlords in the 2010s in Detroit often regarded rental housing as valuable only for the rent they could extract. The houses themselves were seen as largely worthless. A common practice was buying many homes at tax auctions for very low cost, extracting as much rent as possible over the next few years while failing to pay property taxes or maintain the homes, letting the properties fall back to tax foreclosure, and repeating the cycle again with new homes.

So while a homeowner might be owed windfall profits on one house, a speculator or landlord could reap these profits on multiple properties.

The 2015 tax foreclosure auction is revealing. That auction was the largest to date, with more than 25,000 Wayne County properties tax foreclosed. Those who would benefit most from repayment of windfall profits in that auction are not the meager 13 percent of homeowners in the tax auction that year who saw their homes sell for a median profit of $4,400, but the dozens of speculators and landlords with multiple tax foreclosed properties whose median cumulative windfall was $25,000.

To truly address the injustices of Michigan’s foreclosure system, efforts should focus on what most harms homeowners: exorbitant interest rates and, for some, the devastating loss of their homes. The present series of lawsuits has little to do with justice for those wronged by tax foreclosure.

Alex Alsup is vice president of research and development at the nationwide land parcel data company Regrid. Previously, he led national philanthropic housing work at the Rocket Community Fund, the philanthropic arm of Rocket Mortgage. He has researched and written about the Michigan tax foreclosure system since 2011.

Suggested Citation: Alex Alsup, Takings Clause Victory Would Not Fix Michigan’s Tax Foreclosure System, Sᴛᴀᴛᴇ Cᴏᴜʀᴛ Rᴇᴘᴏʀᴛ (May 7, 2024), https://statecourtreport.org/our-work/analysis-opinion/takings-clause-victory-would-not-fix-michigans-tax-foreclosure-system.

Related Commentary

Earning a Living in Arizona’s History

A recent oral argument portends Arizona may be the latest state to reject lockstepping with the federal rational basis test in economic liberties cases.

The Path Not Taken in Federal Takings Law

Debates from 19th century state conventions explain why some constitutions allow takings for “private use.”

"Liberty" is a Big Word, and That’s OK

A recent abortion rights decision in North Dakota demonstrates that the distinction between “fundamental” and “non-fundamental” rights doesn’t always make sense in state constitutional jurisprudence.

Resistance to Public Policies Assisting the Poor

Property owners have challenged programs meant to assist vulnerable populations, alleging they are unconstitutional takings of private property for public use.